By Arun Advani and Andy Summers

Looking at official inequality statistics, the past decade was bad, but it was bad for everyone. As income growth flat-lined, so too – it is often said – did income inequality. We were ‘all in it together’, to use the famous phrase. But official inequality statistics exclude ‘irregular receipts’, in particular capital gains. Once these are added to incomes, the share of resources going to those at the top actually grew substantially, while average incomes stagnated.

The ten years since austerity began have not been easy ones. Productivity, wage growth, housing and crime all worsened, with very real consequences for people’s lives. Income inequality, however, seemed to buck the trend. Whether measured by the Gini coefficient or by top income shares, inequality apparently did not get any worse. But as Aaron Levenstein put it, ‘Statistics are like [swimsuits]. What they reveal is suggestive, but what they conceal is vital.’

In this case, the key concealment is that official income inequality statistics have excluded so-called ‘irregular receipts’, particularly, capital gains (profits received on the sale of assets). When capital gains are included, the picture changes considerably. Capital gains significantly supplement the highest incomes, and this form of remuneration has steadily increased since 2010, allowing those at the top to weather austerity relatively comfortably. Far from being constant, over the past ten years inequality has been rising.

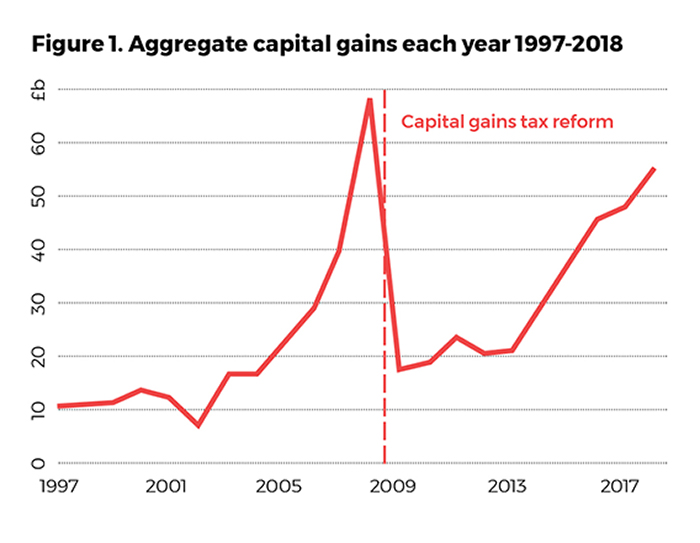

The tax system heavily favours capital gains, which are taxed between 10 and 28%, compared with income, which at the top is typically taxed at 47% but can be as high as 62%. Such favourable tax treatment has spurred growth in capital gains of almost 300% over the last decade, returning aggregate gains to a level last seen just before the Financial Crisis (Figure 1).

Whether this remarkable rise in aggregate gains matters for inequality depends on how these gains are distributed. If they are distributed in exactly the same way as income, then inequality would be the same when measured with total remuneration (income plus capital gains). But they are not.

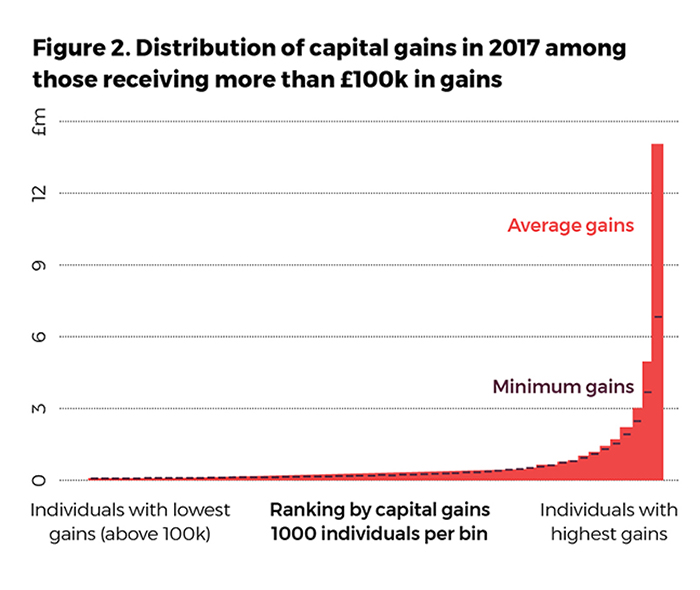

Using confidential administrative data from HM Revenue and Customs (HMRC) covering all tax filers between 1997 and 2018, our research shows that taxable capital gains are extremely concentrated. In 2017, the top 5000 individuals ranked by capital gains (0.01% of UK adults) received 54% of all taxable gains; by contrast, the comparable figure for taxable income is just 2%. Figure 2 shows the distribution of capital gains among those with more than £100,000 in gains. Even within this (very rich) group, the concentration at the very top stands out. The top 1,000 received at least £6.9 million each in capital gains, averaging £14 million. Inequality in capital gains is substantially higher than in income.

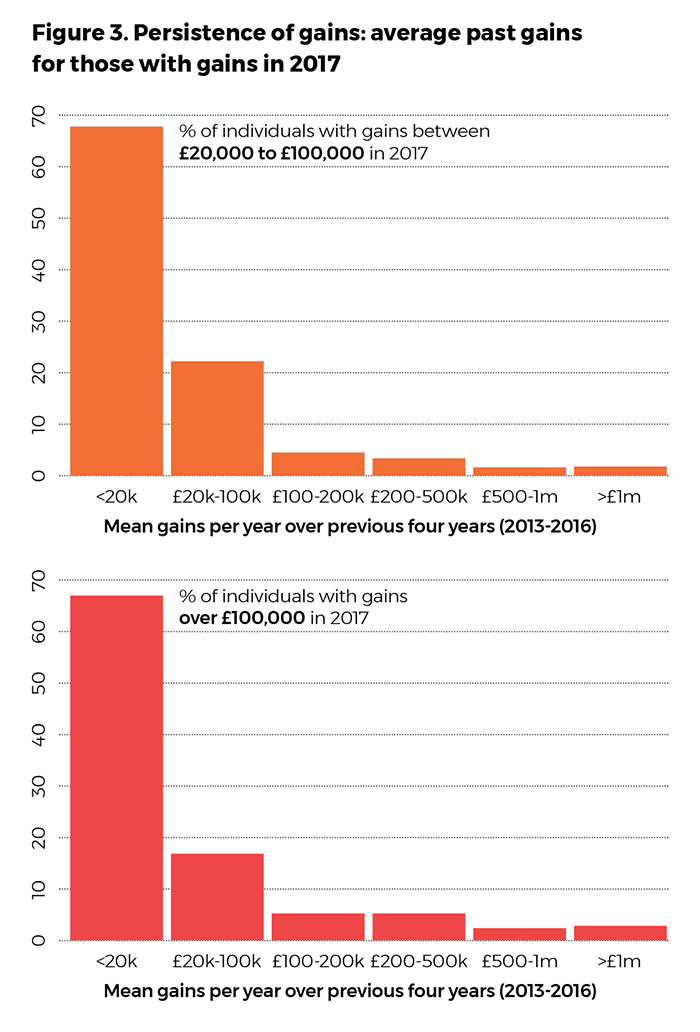

But we should also think about the persistence of capital gains. If capital gains are concentrated but go to a different set of people each year, then from a lifetime perspective their impact may average out. Indeed, the idea that receiving capital gains is a rare event is part of what has motivated its exclusion from usual income statistics—they are treated as an ‘irregular receipt’.

Our research shows that for a substantial minority of the UK’s richest individuals, capital gains are not a rare event, but a regular part of how they receive their remuneration. Figure 3 illustrates that one third of those who received gains over £20,000 in 2017, also received at least this much, on average, over each of the preceding four years. Amongst those with gains over £100,000, one in six had received over £500,000 in total, in the five-year period since 2013.

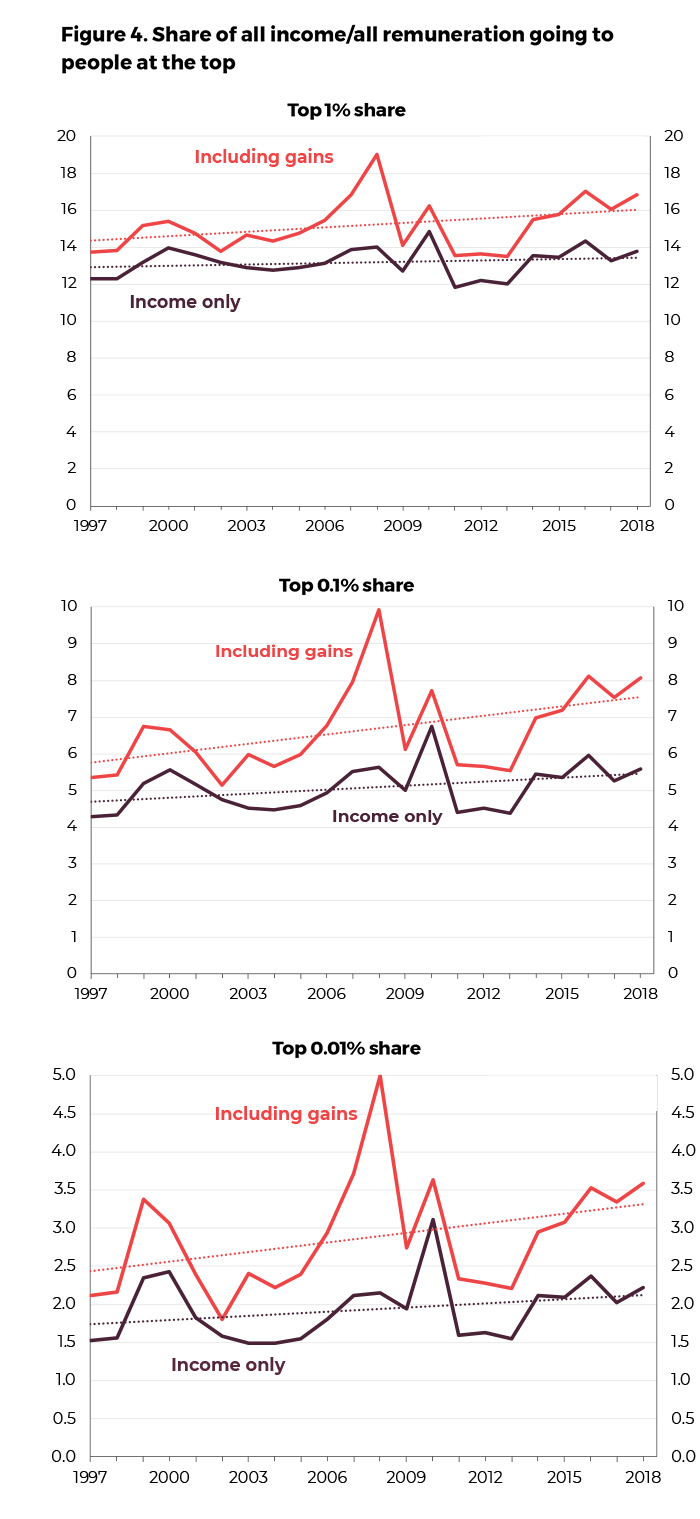

Having seen that capital gains have grown over time, are highly concentrated, and are also persistent for some, it is natural to ask what this means for our understanding of inequality. Figure 4 shows how shares of total income and total remuneration (income plus gains) have changed over the past twenty years. The top panel shows the share for the top 1% of UK adults (roughly half a million people); lower panels repeat this for the top 0.1 and 0.01%.

Looking only at incomes between 1997 and 2018 we see a familiar story: the top 1% share has hovered consistently at around 14% for the past decade, rising slightly between 1997 and the 2008 financial crisis, but hardly increasing since. But when we look at total remuneration including capital gains, we see a very different story. Not only is the top 1% share of remuneration much higher than the income share, but since 2011 it has been increasing. Between 2011 and 2018 the top 1% share of total remuneration rose by more than three percentage points from 14 to 17%; the top 0.1% share grew at an even faster rate, from 6 to 8%.

Including capital gains, the top 1% of UK adults had an average total remuneration of £392,000 in 2018, compared with an average income of ‘only’ £307,000, a 28% difference. In 2011, that difference was only 17%. Looking at even smaller and better-off groups, the effects are even larger: for the top 0.01% (around 5000 people), including capital gains adds (on average) 62% on top of incomes in 2018, compared with 32% in 2011.

Austerity was socially and economically painful for most people, but not for everyone. Although conventional wisdom is that everyone suffered with stagnating incomes during austerity, this masks a big shift in the way that the richest received their remuneration. By ignoring capital gains and focusing exclusively on taxable income, official statistics have missed this major trend in inequality over the past decade, delaying debate about the appropriate policy response.

This article was published in Advantage Magazine: Austerity, 10th Anniversary Special, Summer 2020.

About the authors

Arun Advani is Assistant Professor of Economics at the University of Warwick and Impact Director of CAGE. He is also Research Fellow of the Institute for Fiscal Studies, and Visiting Fellow of the LSE International Inequalities Institute.

Andy Summers is Assistant Professor of Law at the London School of Economics, Associate Member of the LSE International Inequalities Institute and a CAGE Associate.

Further reading

Advani, A., and Summers, A. (2020) Capital Gains and UK Inequality, CAGE policy briefing (no. 19)

Advani, A., and Summers, A. (2020) Capital Gains and UK Inequality, CAGE Working Paper (no. 465)

Advani, A., Corlett, A., and Summers, A. (2020), ‘Who gains’, Resolution Foundation report

This research was funded by the Economic and Social Research Council (ESRC) through the CAGE Research Centre at Warwick (ES/L011719/1) and by LSE International Inequalities Institute, LSE Law, and Warwick Economics. This work contains statistical data from HM Revenue and Customs (HMRC) which are Crown Copyright. The research data sets used may not exactly reproduce HMRC aggregates. The use of HMRC statistical data in this work does not imply the endorsement of HMRC in relation to the interpretation or analysis of the information.