Recession Watch: West Midlands

The West Midlands bears the brunt of the current recession…

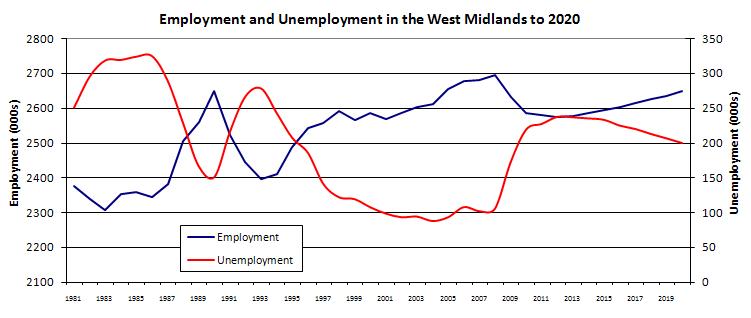

The University of Warwick Institute for Employment Research, one of Europe's pre-eminent centres for labour market research, is keeping a watching brief on the development of the recession and its long-term implications for the University’s host region: the West Midlands. Initial indications point to the region bearing the brunt of the recession. Unemployment, already higher than the UK average for most of the 2000s, has begun to accelerate at a faster than the national one rate. In June 2009, the West Midlands had the highest unemployment rate, measured by the claimant account, of all the regions and nations in the UK.

…this has repercussions for employment long after the recession has ended

The current recession is not like those the economy faced in the recent past - 1974, 1980, and 1990 – because its cause is not rooted in purely domestic issues of high inflation and lack of competitiveness. This time around the recession stems from a worldwide failure of the financial system and the concomitant tightening of the supply of credit (the credit crunch). Despite initial concerns that the current recession was a white collar one, given the focus on the loss of jobs in the financial services sector, the characteristics of job losses appear similar to those of previous recessions: job losses are being concentrated in areas which have a more vulnerable industrial base (i.e. a concentration of activity in those sectors suffering a long-run decline in employment); and it is the less skilled and qualified who are most at risk of being unemployed. More highly skilled people who lose their jobs still stand a better chance of finding work, probably at the expense of those who are less highly qualified and skilled.

What is of interest is how the West Midlands economy will recover from the current recession. Recessions do not, themselves, necessarily bring about structural shifts, but they can accelerate the pace of change. Hence the long run decline in manufacturing employment – which has been in evidence since the 1960s and 1970s – is likely to be accelerated further, with knock-on effects to other industries which provide a range of services to the sector.

The latest Cambridge Econometrics (CE) / IER assessment of future employment prospects, suggests the outlook for the region is relatively pessimistic compared to other parts of the UK. Though employment levels are not expected to fall as much as in previous recessions there is a relatively slow pick up in employment to the year 2020, such that even by then pre-recession levels of employment will not have been recovered.

Over the medium-term the manufacturing sector will decline even further…

By 2020 there is expected to be considerable further change in the industrial composition of employment: manufacturing employment will continue to decline but not as much as it did over the 2000s. Employment growth will be limited mainly to construction and non-marketed services (including some parts of the public sector).

One has to be cautious about inferring too much about the decline in employment in some sectors. Because people will retire or leave an industry for a variety of reasons, there are replacement demands to consider. Once these are take into account, there is nearly always a positive demand for labour. So whilst manufacturing employment will continue to decline overall, there are likely to be significant replacement demands for labour. This raises the problem of how to attract people to work in a sector which is perceived to be in decline.

…with the loss of the skilled jobs traditionally associated with the region

Related to the change in the industrial composition of employment will be changes in the types of job people undertake. There will be a continued decline in the number of people employed in skilled trades jobs – typically those associated with skilled manual work in the manufacturing and construction sectors. This will be offset by a growth in relatively highly skilled jobs (managers, professionals, and associate professionals) and many relatively less skilled ones (caring / personal service occupations). In general, highly skilled jobs are projected to grow less in the West Midlands than nationally; and caring type jobs are expected to grow more. This has been characterised as an increasing polarisation of labour demand with a thinning out of jobs in the middle.

The recession has exacerbated the long-term problems facing the West Midlands economy

The problems which currently beset the West Midlands labour market are not solely a result of the current recession. The root of many of these problems lies further back in the past – but they have been exacerbated by recent events. Pre-recession levels of employment are not expected to recover even by 2020 and higher levels of unemployment than have been experienced over the 2000s are set to remain over the medium-term. These are the latest projections of the current state of play. There is much uncertainty, especially so as the decline in output over the second quarter of 2009 was greater than expected by some. Without doubt, the problems posed by the current recession, whilst challenging for the economy as a whole, are particularly so for the West Midlands.

Further information

Further information about the Institute’s forecasting activities can be obtained from Professor Rob Wilson (r.a.wilson@warwick.ac.uk). Rob Wilson produced the Working Futures research programme which is the definitive assessment used by Government of the UK’s future demand for labour and skills. See http://www2.warwick.ac.uk/fac/soc/ier/research/current/wf. Terence Hogarth (t.hogarth@warwick.ac.uk) has led a programme of research into how the recession has affected different aspects of the labour market.

{kind=link}