Warwick Business School UK Probability Forecasts, Nov 2014

WBS Forecasts for 2014 and 2015

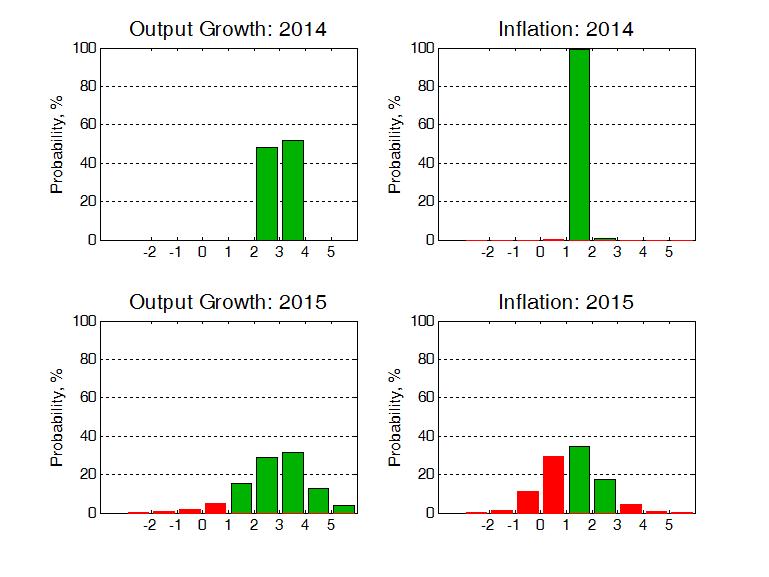

The figure below presents WBS’s latest (as of 26th November 2014) probabilistic forecasts for real GDP growth and inflation – for 2014 and 2015 – as histograms.

“Favourable” outcomes are coloured green; with “unfavourable” ones coloured red. For GDP growth, “favourable” outcomes are defined as GDP growth greater than 1% p.a.. For inflation, “favourable” outcomes are defined as inflation within the Bank of England’s target range of 1%-3%, such that the Governor does not have to write a letter of explanation to the Chancellor.

Inspection of the figure reveals that the balance of probabilities is such that the economic recovery in the UK is set to continue through 2015. But, as the red columns indicate, the WBS forecasting system suggests that there remain downside risks to GDP growth next year with the forecast histogram skewed to the left. This long left “tail” to this histogram indicates that, despite expected growth of more than 3% in 2014, prospects for 2015 remain far from certain - with a 8% probability of “weak” growth of less than 1% (see Table 1 below).

While the most likely forecasted outturns for inflation in 2015 will not involve a letter of explanation from the Bank of England Governor, the risks to inflation are clearly on the downside. This follows UK inflation recently falling to five year lows due to weaker oil, food and import prices. Business and policymakers should remain alert to these downside risks

Event Forecasts

From the WBS forecast histograms we extract the following forecasts.

Table 1: Probability Event Forecasts for Annualised % Real GDP Growth and CPI Inflation

|

Year |

Real GDP Growth (%, p.a.) |

CPI Inflation (%, p.a.) |

||||

|

|

Prob(growth<0%) |

Prob(growth<1%) |

Prob(growth<2%) |

Prob(letter) |

Prob(CPI<1%) |

Prob(CPI>3%) |

|

2014 |

<1% |

<1% |

<1% |

<1% |

<1% |

<1% |

|

2015 |

3% |

8% |

23% |

48% |

42% |

6% |

Table 1 shows that, despite the expected continuation of growth in 2015, there remains about a one-in-four chance that GDP growth will be less than 2%. This heightened uncertainty about the prospects for economic growth in 2015 implies that one cannot presume that annualised growth will pick up to historically “normal” levels of between 2% and 3% p.a..

The WBS forecasting system emphasises that the risks to a breach of the inflation target in 2015 remain high – close to a one-in-two chance. This is because the probability of inflation falling below 1% in 2015 has risen sharply from 13% a quarter ago - to the current expectation of 48% - as oil, food and import prices have fallen in recent months.

Comparison with other forecasters

The main objective of the WBS forecasting system is to provide benchmark and judgement-free probability forecasts; and to assess the risks associated with other forecasts when these do not involve a direct communication of forecast uncertainty.

Accordingly, we take the most recent forecasts from the IMF, the Bank of England and HMT’s Panel of Independent Forecasters. While the Bank of England does provide an explicit assessment of forecast uncertainties for the UK, via “fan charts”, the IMF and the HMT Panel provide point forecasts only.

We use the WBS forecasting system histograms to compute the probability that GDP growth or inflation is greater than the other forecaster’s “point” forecast. If the point forecast from the other forecaster falls in the centre of the WBS forecast distribution we would expect this probability to be 50%. On the other hand, if the forecaster is more optimistic (pessimistic) than we suggest they should be the probability will be less (greater) than 50%.

Table 2: Forecast Comparison for 2015

|

|

Real GDP Growth (%, p.a.) |

CPI Inflation (%, p.a.) |

||

|

|

Point Forecast |

Prob. of a higher outturn |

Point Forecast |

Prob. of a higher outturn |

|

IMF |

2.7 |

58% |

1.8 |

28% |

|

Bank of England [1] |

2.9 |

54% |

1.2 |

51% |

|

HMT Panel [1] |

2.6 |

62% |

1.9 |

24% |

While the IMF, Bank of England and HMT Panel forecasts for GDP growth in 2015 fall close to the centre of the WBS forecasting system distribution, the IMF and the HMT Panel expect higher inflation outcomes than the WBS system. Inflation is therefore likely to fall below their expectations.

Note on the Warwick Business School Forecasting System

The Warwick Business School Forecasting System communicates forecast uncertainties for UK GDP growth and inflation in an open and transparent way – free from judgement. The system involves consideration of a range of cutting-edge econometric forecasting models, as opposed to relying on a single model which is likely misspecified.

Focus is on the production and publication of accurate probabilistic forecasts, using statistical methods, rather than constructing a narrative or story around one particular, but likely far from certain, possible set of outturns.

The WBS forecasts thus emphasise forecast uncertainties; and provide a benchmark against which one can assess the plausibility of other forecasts. A note summarising the System, and evaluating its historical performance, is available at this link.[1] The Bank of England (mean) forecasts for calendar year inflation are derived from their published forecasts for the four-quarter inflation rate and are, therefore, to be treated as approximate. The HMT Panel (mean) forecasts for inflation are four-quarter growth rates.